Investing in Our Mission

A Five-Year Case Study of Fossil Fuel Divestment at the Rockefeller Brothers Fund

Since committing to fully align our investments with our mission, the Rockefeller Brothers Fund has cut fossil fuel exposure to less than one percent of our portfolio. Financial performance over more than five years has outstripped the market benchmark.

Introduction

Putting All Our Assets to Work Toward Our Goals

by Stephen B. Heintz, president

We knew our announcement, planned for the day after more than 600,000 people would take to the streets for the People’s Climate March, would be big news. The family philanthropy rooted in John D. Rockefeller's oil fortune was going to divest from fossil fuels. Still, when the day came on September 22, 2014, the extent to which our decision captured headlines—and the public imagination—genuinely surprised us. Major papers and prominent news programs in the United States and around the world embraced the story. The Rockefellers were getting out of oil.

In truth, by the time we reached that juncture five and a half years ago, the idea that our investment portfolio should not include fossil fuel companies no longer felt extraordinary or surprising to those of us charged with leading the Rockefeller Brothers Fund (RBF) into the future. On the contrary, what had ceased to make sense to us was for the RBF endowment to own companies whose success directly challenged a key part of our mission: to create a more sustainable world.

When I joined the RBF in 2001, I quickly became familiar with a notion common among large endowed foundations: Philanthropic programs were to be kept separate from the financial management of the endowment by a “firewall” meant to keep the two functions apart.

There are, to be sure, some good reasons for this approach. The skill set needed for sound management of grantmaking in furtherance of an organization’s mission is very different from the skill set needed by money managers. If the financial stewards do their jobs right, there’s more funding for programs; if they do poorly, the whole enterprise may fail.

Still, arriving as a relative outsider, I never fully bought into this idea of a firewall between those who managed the money and those who ran the programs. I embraced the imperative for money management to be in the hands of capable professionals with appropriate skills. I saw the clear importance of bringing rigor and caution to the investment process. Three successive generations of Rockefeller family members have refined and advanced the RBF’s mission in the past three-quarters of a century, and the board intends for future generations to have the means and opportunity to do this work as well.

What I did not accept was the premise that careful stewardship of our endowment required that we insulate management of the portfolio from the broad mission of the organization as a whole. I didn’t see why our goals—the overarching purpose of the RBF—should only be visible to and achieved by people working on one side of the firewall.

With a 2020 grantmaking budget of about $39 million, the RBF is a modest-sized foundation. But we have big ambitions. We have always explored how we can further leverage all our assets—not just our endowment, but our name, our history, our convening power—to advance our mission. We had been examining the impact we might have with our endowment monies for the better part of a decade before we moved to divest. In that time, we became convinced that it should be possible to pursue our mission not just with the approximately five percent of our endowment money that we devote to programs each year, but also with the 95 percent we have invested in capital markets to finance our activities in the future.

The RBF made a $12.5 million impact investment in Renewable Resources Group (RRG). Its portfolio companies include Homer (left), which improves the resilience of California's water system; California Harvesters (center), an employee benefit company that company restructures the typical farm labor contract to provide a better working environment; and Tule Fog Farms (right) where RRG planted 1,680 acres of almonds and pistachios between 2013-2014.

Our first step was an effort to be more active shareowners, and we adopted guidelines in 2005 for how we would vote the shares the endowment held. Our next move was to commit 10 percent of our endowment to impact investments that both made measurable contributions to social change and provided market-rate financial returns with risk levels similar to other components of the portfolio.

Still, we had the moral discomfort of owning fossil fuels in our endowment while focusing much of our grantmaking on the challenge of climate change. But the groundwork for doing something more had been laid. We had sharpened our focus on what we intended to do with the endowment and what was possible. We had overcome initial resistance from our investment committee. And we had found the right partner in our new money management firm, Agility, which committed to working with us in the effort to better align our investments and our mission. By late 2014, the RBF was ready to get out of oil.

In the more than five years since we began to shed our fossil fuel investments, our endowment performance has not suffered from our divestment commitment. In fact, returns have exceeded expectations and beaten the benchmarks we use to measure our investing success.

We were not the originators of fossil fuel divestment or mission-aligned investing. We learned a great deal from others and took a chance on some very smart people and quality research. Once the decision was made, we moved carefully and deliberately, aiming to be transparent at each step along the way. From the beginning, we wanted to share our lessons and explain our motivations, recognizing the potential that existed in helping to create a movement. We believed that our leadership in this area could multiply the impact that our modest pool of capital might have. We offer this detailed case study of the RBF’s experience since 2014 in that spirit.

Today, others can move more quickly than we did. Any foundation or endowment or other investment pool that has not yet taken the initiative to align its investing practices and its values can take advantage of our experience and of the examples set by many others that have already gone through the divestment process. Our hope is that this report adds a bit more shared knowledge on these topics as the movement continues to gain momentum.

—March 2020

The Bottom Line: Financial Outperformance

Divestment has been a success for the Rockefeller Brothers Fund. We now have more than five years of financial data that can be used to assess how our endowment has performed under the commitments made in 2014 to rid our portfolio of fossil fuel investments and more fully align our endowment with our mission.

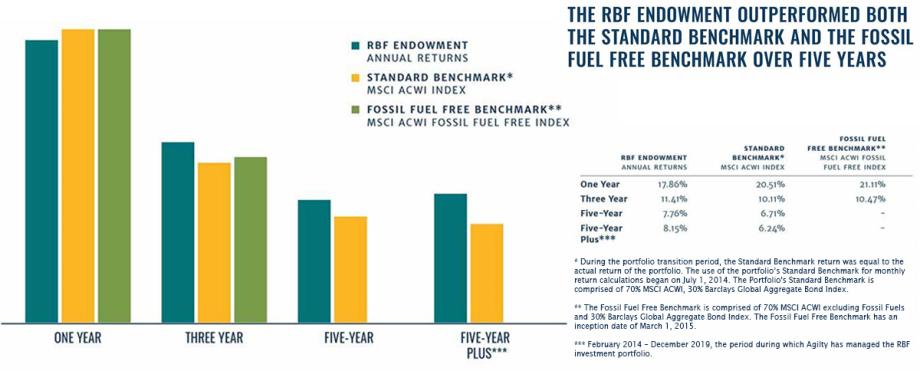

Financial results in this period have exceeded expectations. The RBF investment portfolio beat its performance targets, posting an average annual return of 7.76 percent over the five-year period that ended December 31, 2019. Over the same period, our benchmark investment portfolio, made up of 70 percent stocks and 30 percent bonds, returned only 6.71 percent annually.

The Journey

Finding the Right Partners

The RBF leadership had for some time been examining how to go about aligning the investment portfolio more fully with its philanthropic mission. The efforts included the adoption, in 2005, of guidelines for voting the stock that the RBF owned in its endowment and for deciding when to support or oppose specific shareowner resolutions. In 2010, the RBF engaged in a new effort to allocate up to 10 percent of its endowment to impact investments.

Work on these initiatives helped deepen the RBF's knowledge of mission-aligned investing and make its leadership and investment committee more comfortable with the idea that the endowment might be managed for goals beyond just the highest possible returns.

The RBF’s active share ownership initiative, which led to the guidelines for how to vote shares owned in the endowment, began at a time when the investment committee was directly involved in the selection and management of its holdings, finding and making actual investments for the endowment. But just a few years after the share voting policy was put in place in 2005, the RBF moved to an outsourced chief investment office (OCIO) model.

An OCIO selects and manages all the investments that go into the portfolio, leaving the foundation’s staff, trustees, and investment committee with streamlined approval and oversight tasks. According to Geraldine Watson, RBF executive vice president for finance and operations, the first OCIO the RBF hired did not manage the endowment as a separate account. Rather, investments were commingled with that firm’s other clients. This offered the benefits of a deep bench of investment professionals, access to a wider range of fund managers, and cost efficiencies, she says, but the pooled-fund structure hindered any customization of the endowment.

“As time went on and we sought to further integrate our philanthropic priorities into our investment strategies, we recognized this commingled model created significant obstacles to implementing our mission-aligned investing goals,” Watson says. “Because any action in a commingled investment would require buy-in from all the pooled investors, it was difficult to vote the proxies for shares that the RBF owned, source impact investing vehicles, or exercise discretion as to investments we wanted to access or avoid.”

Neva Goodwin, the daughter of RBF cofounder David Rockefeller and former vice chair of the board of trustees who was instrumental in the effort to develop the proxy voting policy, says hiring the first OCIO scuttled implementation of the guidelines. “Our entire process ended with a thud,” she says.

Neva Goodwin on:

Getting Consensus

“There often will be differences between the investment committee and the rest of an organization’s board or leadership. The investment committee is likely to say that its job is to maximize returns, while the rest of the board may say, wait a minute, our impact as an organization can be greater if we exert the power of our investments. This tension certainly existed within the RBF. It was hard work to develop our active shareholder initiative, but the consciousness-raising we all experienced by doing that work was very useful. The thinking on our endowment has had a great evolution since that time. And I think divestment has been more impactful than anything we tried before.”

Neva Goodwin is an economist and a distinguished fellow at the Boston University Global Development Policy Center. The daughter of David Rockefeller, she served as vice chair of the RBF board of trustees until 2009.

In 2013, the RBF began a search for a new money manager. “As we did our search, we knew that we no longer wanted our investments to be pooled with a firm’s other clients,” Watson says. “We needed customization of our portfolio management with separate accounts. We wanted active partners on our mission-aligned investing goals.”

In early 2014, the RBF brought on Agility as its new OCIO. Chris Bittman, Agility’s chief executive officer, says that when his firm was hired, his managers and analysts did not have all the skills and knowledge they would need to do what their new client wanted. “But we made a commitment that we would build that expertise, and we have.”

Agility committed to managing the RBF endowment as a separately managed account, rather than a commingled fund. Fairly quickly, the firm was able to start bringing the endowment more impact investing opportunities. The new OCIO also began shedding some of the portfolio’s fossil fuel positions almost immediately, even though the formal divestment decision didn't come until later in the year.

“The work we did was useful in the end,” Goodwin says of the proxy voting initiative, “because it started the process.” That process complemented work that Goodwin and other members of the Rockefeller family had done, independently of the RBF, to challenge Exxon Mobil to address climate risks. In 2008, the Rockefeller family used its name to help push a series of shareholder proposals, including the request to appoint an independent chairman, but the effort failed.

All this earlier activity helped sow the seeds of the much more comprehensive mission-aligned investing effort that the RBF has today—including, in some instances, active share ownership in line with the policy Goodwin helped develop a decade and a half ago.

Today, Bittman points out, the incentive structure within Agility is built so that every professional at the firm is rewarded based in part on the portfolio performance outcomes for clients—including goals for portfolio mission alignment for the RBF and others.

Defining Goals

“The first step is defining what mission alignment means for the client,” says Jameela Pedicini, who was cohead of mission-aligned investing at Agility from 2015 to 2019. “There’s no one right answer, but rather a spectrum of possible approaches and toolkits to utilize.”

One foundational change that the RBF made as it set about focusing its mission-aligned investment effort was to rewrite its return objectives. “It had become clear at that point that we had two mandates,” Watson says. The longstanding commitment to preserve the endowment in perpetuity still stood, now tempered by the directive to align investments with the organization’s mission.

The previous return objective stated: “The investment portfolio will be managed to maximize annualized returns net of all costs over rolling 10-year periods while adhering to the Fund’s stated risk parameters.” The new version said: “The Fund’s long-term investment objective should be to preserve the real value of the endowment.”

This might seem subtle, but it was an important change. The new wording about preserving the real value, Watson explains, provides the endowment’s managers and the investment committee with more latitude to consider various attributes of an investment beyond its potential for the highest possible returns. And it means the endowment is managed in a way that seeks to ensure that the RBF can keep up with its five percent annual spend—mandated under tax rules for U.S. philanthropies—plus inflation, investment management fees, and taxes.

Vision Ridge Partners, one of the RBF’s largest impact commitments, invests in sustainable real assets. Portfolio companies Sun World International (left) breeds non-GMO grapes that achieve greater yields with fewer resources, Vanguard Renewables (center) runs anaerobic digesters to turn manure and food waste into energy, and Guzman Energy Group (right) delivers renewable power tailored to Colorado and New Mexico.

The New Math of Stranded Assets

Leading climate organizations and activists, many of whom were grantees, had approached the RBF about joining the divestment movement, but the investment committee was naturally reticent to commit to any rules or practices that might hurt long-run returns.

“Endowment managers are temperamentally some of the most conservative people,” says Michael Northrop, RBF program director for sustainable development. “We needed to have a generational shift on that committee before we were really able to have a conversation about divestment.”

Mark Campanale on:

Why Energy Companies Have Farther to Fall

“The financial models supporting the stock market valuations of oil and gas companies are still based on business as usual—namely, an expectation of continuing growth in oil demand. But fossil fuel divestment and a growing awareness of the stranded asset risks are chipping away at the margins of this consensus view. A few companies have written down assets on climate grounds, conceding that reserves were going to get stranded. Most Wall Street analysts are just beginning to understand the significance of the clean energy transition and the electrification of transport, in particular; their valuation modeling has yet to reflect the new reality. While we haven't yet seen investors collapse the carbon bubble, oil and gas companies are trading at historic lows as investors flee the chaos. Energy companies have gone from 15 percent of the S&P 500 a decade ago to now less than four percent. The real question is whether the sector will ever recover, or whether it has much farther to fall as skepticism about fossil fuels’ future spreads across financial markets.”

Mark Campanale is the founder and executive chairman of Carbon Tracker Initiative, which in 2011 published “Unburnable Carbon: Are the World’s Financial Markets Carrying a Carbon Bubble?”

Changing the attitudes of investment committee members to make them more open to using the endowment to further the RBF’s mission was a process that took patience. Efforts to bring new people into the process by introducing committee member term limits and focusing on diversity spanned more than a decade before Agility assumed the role of OCIO in 2014.

The committee asked Agility to perform a backward-looking analysis of market returns for the RBF. The findings were bleak: They suggested that a portfolio stripped of fossil fuels would have dramatically underperformed the broader market in the past.

But it was becoming clear that the past would not be indicative of the future, and companies whose valuations depended on their holdings of oil, gas, and coal might be vulnerable.

A new math, based on an analysis of global fossil fuel reserves by Carbon Tracker Initiative, a London-based group funded in part by the RBF, showed that most of those reserves would need to stay in the ground to stem the rise in global temperatures. These unburnable reserves, already on the energy producers’ books, had a real chance of eventually becoming stranded—unproductive assets for the company and worth nothing in the market—as the world grappled with how to address the climate crisis.

Because the market value of energy exploration and production companies is closely tied to their coal, oil, and gas reserves, the potential stranding of these assets would indicate that the companies themselves were overvalued. Valuations should, at some point in the future, collapse—meaning an investment in the companies today is riskier than most people realize.

“We felt divestment was the morally right thing to do,” says RBF President Stephen Heintz. “But we were more than a little bit nervous. We wanted to demonstrate that we could remove fossil fuels from the portfolio and be financially prudent as well.”

The stranded assets thesis provided reassurance to the RBF board and investment committee that, despite the anxiety-inducing backward-looking analysis, there were financially sound reasons to divest in addition to the moral arguments.

“Carbon Tracker’s analysis helped give me the confidence to move forward,” Heintz says. Coming to see fossil fuel reserves as a “carbon bubble,” rather than as a sound metric for stock valuation, was a critical turning point. “It helped us to persuade our investment committee that we weren’t just taking a moral stand but might also be adopting a smart financial stance.”

Hugh Lawson, RBF investment committee chair, says the RBF also believed that the process of decarbonization needed to be more rapid. “We concluded it was important for us to help show the way by creating a portfolio that was not reliant on fossil fuel extraction for returns,” he says.

The Bottom Line: Getting Out of Fossil Fuels

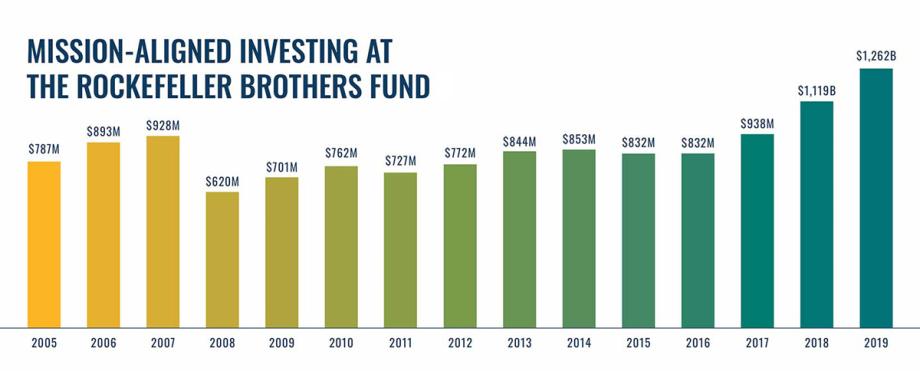

The RBF’s divestment pledge in 2014 began a process that, five years later, has all but eliminated coal and tar sands from the endowment and dramatically reduced total fossil fuel exposure. Our mission-aligned investing initiative has greatly expanded the organization’s impact investments, which are now on track to become 20 percent of the portfolio within a few years.

When Agility completed the first comprehensive analysis of fossil fuel exposure in the RBF endowment, carbon-intensive coal and tar sands were 1.6 percent of the portfolio, and total exposure to all fossil fuels stood at 6.6 percent. At the end of 2019, coal and tar sands were just 0.05 percent of the portfolio. Total fossil fuel exposure had been reduced by about 80 percent to less than 1 percent of all investments.

The RBF Portfolio Today

Fulfilling the Divestment Pledge

The commitment that the RBF made in September 2014 promised elimination from the portfolio of all exposures to coal and tar sands, which are particularly carbon-intensive energy sources, and then an examination of how best to purge oil and gas from the endowment.

To cut fossil fuel exposure, mutual funds, exchange-traded funds, hedge funds, and other investment vehicles that own the stocks or bonds of energy producers—or any company, regardless of industry, that holds fossil fuel reserves—have been sold.

Private market investments in vehicles that may include oil or gas reserves have in some cases been sold. The RBF had to decide what to do with existing, illiquid private real asset holdings that had links to traditional energy in them. It would have been possible to sell all or most of these, Bittman says, but in some cases that would have resulted in steep losses.

“This was a tough decision where we had to balance our dual mandate of investment returns and mission alignment,” Watson says. “It wasn’t easy, but for the small slice of our legacy investments that are exposed to fossil fuels, we ultimately determined that letting them run off would be the better choice for our long-run financial stability and still move us on the path toward full divestment.”

The 0.9 percent of the endowment that still does have fossil fuel exposures—the legacy investments that are running off—is a subset of assets categorized as traditional, meaning they do not have explicit agreements preventing managers from holding fossil fuels. Traditional investments account for 31.6 percent of the RBF investment portfolio. New investments in this category are assessed to determine that they do not hold fossil fuel reserves and are not involved in fossil fuel industries. A fund that invests in biotechnology stocks, for example, may not be accompanied by a specific agreement with the manager to exclude fossil fuels, but the definition of the fund’s investment objectives will all but guarantee such an exclusion.

To determine which public companies worldwide hold coal, oil, and gas reserves and are therefore ineligible for the RBF endowment, Agility relies primarily on the MSCI Fossil Fuel Reserves Screen. This identifies almost 400 companies, across a variety of industries, that own fossil fuel reserves. That’s out of a total universe of about 8,500 securities in the MSCI All Country World Index that the RBF uses as its equity benchmark.

While screening for reserves doesn’t specifically exclude all energy industry participants, such as oil tanker companies or oil services providers that don’t control any reserves, Agility tries to avoid adding those to the portfolio, too, according to Tamara Larsen, executive director and head of mission-aligned investing at Agility. “As an example, a traditional private infrastructure fund, which would have meaningful exposure to the midstream pipeline market, is not something that is appropriate for the RBF,” Larsen explains.

New investments Agility has added to the portfolio have, when needed, a side agreement that commits the fund manager to avoid fossil fuels in the investment vehicle or share class that the RBF owns. This group of investments is categorized as screened divest. It comprised 35.4 percent of the portfolio at the end of 2019.

Agility’s commitment to managing the RBF endowment as a separate account, rather than having it commingled with other clients, makes it possible to implement the side agreements and other structures that are often necessary to ensure that an investment is and remains fossil fuel free. An endowment such as the RBF’s is structured as a fund of funds, which makes it possible to benefit from investment strategies run by many different managers. In some instances, the managers need to agree that they will not, under any circumstances, invest in fossil fuels before their investments can be included in the RBF portfolio.

The demand for a fossil fuel free side agreement or commitment from a money manager keeps the RBF endowment from being able to invest in certain funds that might otherwise be attractive, according to Agility’s Bittman. Some managers, even if they have no intention of having any fossil fuel exposure in their funds, will be unwilling to accept restrictions on their investment choices.

In 2016, the Rockefeller Brothers Fund made a $12.5 million impact investment in Mainstream Renewable Power. Its Africa joint venture Lekela Power developed West Africa’s first utility scale wind farm in Senegal.

Impact Investing

Participants in the fossil fuel divestment movement have recognized from the start the value of proactive investment in the companies and technologies that will ultimately replace the most carbon-intensive activities in the economy. This forms a natural complement to the decision to divest and, in announcing its divestment decision in September 2014, the RBF also explicitly pledged further support for clean energy development.

In fact, at the RBF, the commitment to pursue impact investments in clean technologies and other areas aligned with the organization’s goals predated divestment by several years. The RBF made its initial pledge to devote up to 10 percent of the endowment to impact investments in 2010.

The goals, both financial and social, to be pursued through impact investments had to be defined anew when Agility took over the portfolio. A distinguishing aspect of the RBF's impact investing goals was the requirement for all such investments to meet market-rate return and risk attributes without any “lowering of the bar.” This was not a decision to accept lower returns.

Valerie Rockefeller on:

The Impact of the Rockefeller Name

“It was clear to us that there was power in the name—that we could get attention for the divestment movement from many traditional investors just by virtue of our name. Still, I was totally surprised at the level of media interest when we made our announcement. News outlets were eager to run with the story that the heirs to the oil industry’s oldest and biggest fortune were getting out of oil. On MSNBC, Chris Hayes introduced me for an interview by referring to the “epic irony” of the divestment move. I replied that we embrace that irony.”

Valerie Rockefeller is chair of the RBF board of trustees, the first member of the fifth generation of the Rockefeller family to hold that role.

Some foundations have decided to use program-related investments (PRIs) to further their philanthropic goals, extending financing to business projects with clear social benefits where the expected returns might be less than the market rate or the risk of losses higher. These are also sometimes called concessionary investments, because of the lower return expectations. The RBF made an early decision, however, not to engage in PRIs. The impact investments in the RBF endowment are meant to help it survive in perpetuity and finance future philanthropy, just like any other investment in the portfolio.

“Our grantmaking work is very effective, and it’s important to the board that we continue to fund it fully,” says Valerie Rockefeller, chair of the RBF board of trustees. “That includes democratic practice and peacebuilding, which are integral to our mission alongside sustainable development.”

The pursuit of market-rate impact investments at the RBF is meant to support the idea that the philanthropy will continue to exist for future generations and to reflect a belief in the importance of the ongoing programmatic work the organization does. Watson says that the RBF also recognized that it could provide an important example of how investments aligned with one’s values could nonetheless compete, on equal financial footing, with other investment options. “If successful, such an example might encourage more capital to pursue such aims,” she says.

This was an opportunity to take a leadership role and demonstrate to other foundations and endowments that fossil fuel divestment and mission-aligned investing could be done without sacrificing returns, Rockefeller says. This ability to “prove the case” would have been lost had the RBF compromised on what constituted an acceptable level of investment return.

Initially, after the 2010 decision to pursue impact investments, the RBF made slow progress in finding appropriate opportunities. This was attributable to the commingled business model and the investment emphasis of its first OCIO. The pace of impact investing in the endowment picked up meaningfully after Agility became OCIO in 2014—so much so that, in 2016, the board raised the target for impact investing to 20 percent of total assets.

The RBF had committed 14.1 percent of endowment assets to impact investments as of December 31, 2019. Because the impact investments are in primary capital—private equity, debt, and real assets such as real estate and infrastructure—they typically involve an initial commitment of money, with the full investment sum put to work over time. At the end of 2019, assets deployed for impact investments stood at about half of the commitment amount.

The RBF’s impact investments include $12.5 million in Elevar Equity, which helps entrepreneurs meet basic human needs. One of its portfolio companies, Samunnati, provides financial and social capital to small farmers in India. Another, Varthana, makes loans to increase access to education in India.

Environmental, Social, and Governance Factors

As part of the mission-aligned investment process, the RBF endowment seeks funds that proactively consider environmental, social, and governance (ESG) criteria. This applies primarily to the selection of publicly traded companies. The ESG category accounted for 22.7 percent of the endowment at the end of 2019.

Screening with an ESG lens allows the RBF to better align its investments with its mission. But it also can serve as a way to screen for better run companies—businesses more likely to enjoy long-term success. Companies with good governance practices, for example, may be less prone to making bad business decisions. Strong environmental practices, including efforts to reduce carbon emissions or understand and disclose climate change-related risks, may give a company a competitive advantage. This is a principle already reflected in the rationale for divestment, but it can play out more broadly.

Lawson points out that the RBF has long embraced active management for its endowment, as opposed to allocations to passively managed index investments. Insofar as ESG criteria may help in the selection of funds likely to produce better returns, ESG investing is a natural fit for the RBF endowment. Still, the criteria that would qualify an ESG investment had to be identified.

“We engage with managers who are selecting companies with an ESG lens,” says Larsen of Agility. “We evaluate the metrics they are using, the level of engagement they have with companies, how long they may be willing to wait for a company to respond on the key issues they have identified, and more.” Agility believes that this is likely to result in more profitable investments along with better alignment with the RBF’s goals, Larsen says.

The RBF also remains committed to using the voting power of the public company equities that it owns. The transition to Agility as the OCIO for the endowment in early 2014, with the commitment to run it as a separately managed account, made this possible. The RBF adopted an updated set of proxy voting guidelines in 2016 based on the earlier guidance that Goodwin’s committee developed. These guidelines are used when the structure of an investment in the portfolio makes it possible for the RBF to dictate how shares will be voted. In other instances, the selection of an investment based on ESG factors may reflect the manager’s intent to vote shares a certain way, which Agility perceives as being broadly aligned with the RBF’s active shareowner guidance.

Key issues on which the RBF directly or the managers of individual portfolio investments have voted shares include political spending and lobbying, executive compensation, diversity and gender pay equity, and human rights, according to a 2018 review. For investments in the endowment’s ESG category, Agility has managers respond to a questionnaire that asks about the ESG factors they embrace, including priorities the RBF has identified in its mission-aligned investing efforts. A manager’s activities may include voting shares or weighing in on shareowner initiatives, but they often go further and involve active engagement with a company on ESG issues.

Hugh Lawson on:

The Need for Capital Markets to Tackle Climate

“As the RBF contemplated its divestment decision, one of the motivators was our growing feeling that capital markets needed to contribute to the trend toward accelerating sustainability and decarbonization. Few investment managers at the time were willing to offer either fund products that excluded fossil fuels or investable opportunities to build alternative energy solutions. At first, several managers would not agree to a fossil fuel free option for the RBF. But an increasing number of fund managers are now offering these opportunities; some have even come back to us after creating fossil fuel free sleeves to meet growing demand.”

Hugh Lawson is chair of RBF’s investment committee and a partner at Goldman Sachs, where he directs ESG efforts at Goldman Sachs Asset Management.

Financial Performance

As is common with investment funds, the RBF measures its gains against generic indexes to assess whether performance simply reflects a strong period for the markets or is indicative of good investment management. The RBF endowment uses a benchmark that is 70 percent a global equity index and 30 percent a global fixed income index. With an average annual net return of 7.76 percent over the five years that ended on December 31, 2019, the RBF investment portfolio beat the blended benchmark’s 6.71 percent annualized net return by a full percentage point. The RBF portfolio has also shown less volatility than its benchmark, with annualized standard deviation that is 27 percent less than the 70/30 global stocks/bonds yardstick, meaning it has had smaller swings and may be considered less risky.

The financial outperformance of the RBF endowment is even greater when examining the slightly longer period beginning in February 2014, when Agility took control of the portfolio. The RBF investment portfolio posted an average annual net return of 8.15 percent from February 2014 through the end of 2019, putting the outperformance versus the benchmark at nearly two percentage points per year.

“We’re really pleased by the outperformance,” Bittman says. “And the benchmark is not a slow rabbit,” he adds. Bittman means that a 70/30 mix of global stocks and bonds is a relatively aggressive, or growth-oriented, performance yardstick. (He does strike a note of caution that a five- or six-year period is a relatively short time span for establishing an investment track record.)

Bittman also says that the RBF endowment happened to have great timing when it began to sell its fossil fuel holdings in 2014. Crude oil was above $100 a barrel in the first half of the year, and then the benchmark futures price plunged, ending 2014 at about half that level. Energy prices fluctuated in the years that followed, and avoiding fossil fuel investments has had a mixed or limited impact on the portfolio in the period through the end of 2019.

“We recognize that we chose divestment in a period where the price of oil has steadily declined as a function of increased supply,” says Lawson. “But we have also seen a notable increase in the intensity of conservation efforts and in the adoption of renewable fuels, which, at the margin, is beginning to decouple the linear relationship between GDP growth and carbon emissions.”

Lawson sees more asset owners focused on measuring and mitigating carbon transition risk in their portfolios and a growing number who have reduced or eliminated their most carbon-centric holdings. “Cumulatively, these factors reinforce our conviction to underweight companies with a preponderance of their earnings from fossil fuel extraction.”

In the first quarter of 2020, as the COVID-19 pandemic abruptly ended the long bull market and sent stocks into a tailspin, it appeared that not owning fossil fuel investments continued to be an advantage. A 70/30 global stocks/bonds benchmark that uses a fossil fuel free version of the equity index fell 14.31 percent in the first quarter, while the standard benchmark (using an index that includes fossil fuel companies) fell faster, losing 15.05 percent. The RBF endowment declined 11.18 percent, less than either of these benchmarks, during the market turmoil through the first quarter of the year.

The likelihood that fossil fuel holdings will become an ever-greater drag on the valuations of energy producers helps make Heintz and others optimistic about the prospect of continued outperformance by the RBF’s fossil fuel free investments. Heintz believes the markets are still in the early stages of how divestment—or, more generally, a reluctance on the part of investors to risk capital on something that may become a stranded asset—is going to affect the valuations of energy companies. “But it’s accelerating,” he says.

The experience of the coal industry—perhaps the oil industry’s canary in the coal mine, so to speak—may show how the carbon bubble could burst, Heintz says. Coal stocks have been a terrible investment for many years. When Peabody Energy filed for Chapter 11 bankruptcy in 2016, among the issues the company cited was its difficulty in raising capital. At the end of 2019, the reorganized company, once the largest private-sector coal company in the world, had a market capitalization of less than $1 billion.

As much as the outlook for fossil fuel investments in a world confronting a growing climate crisis may be dark, the outlook for renewables and other green technologies appears bright. The RBF endowment has now deployed or committed an estimated 10.75 percent of its assets to investments in companies advancing a low-carbon future. Even before the RBF hired Agility as its OCIO, the firm had selected some renewable energy investments for inclusion in other clients’ portfolios simply based on the expectation of attractive returns—not because the clients were asking for impact investments. Bittman says there is a growing number of attractive green investment opportunities today, though also numerous investments in the category that he says he wouldn’t touch.

Chris Bittman on:

Setting Expectations

“The notion that fossil fuel assets are going to be stranded may be spot on. I believe it’s true, but then the issue becomes what’s the time period over which that happens and when will it be reflected in stock prices. It might happen in two years, but it also might be 20 years. I tell clients I work with that divestment might help performance or hurt performance, but we’ll find out together. I also tell them we’ve gone out and found affirmative impact-oriented strategies with measurable ESG criteria that have outperformed. That’s a great story to tell.”

Chris Bittman is chief executive officer and chief investment officer at Agility.

The Environment for Change

Building a Movement

In divesting from fossil fuels and investing in activities aligned with the organization’s mission, the RBF has been keenly aware of the potential to amplify the impact of its actions by working in coordination with others—by being part of a movement. Since the beginning, the RBF has supported and collaborated with the broader divestment movement, recognizing that this will leverage the impact of its own modest pool of capital. The RBF has been as transparent as possible about its decisions, motivations, and definitions, as well as its investment processes and results, aiming to provide practical information to spur other groups to join the effort.

Early actors in the divestment movement played a vital role in catalyzing the RBF. Especially in the run-up to the divestment decision, individuals and organizations shared their experiences and knowledge to encourage the RBF to divest—and to get the Rockefeller name on the list of those who had decided to get out of oil. Ellen Dorsey, executive director of the Wallace Global Fund who had been working with students and climate activists to help shape the nascent fossil fuel divestment movement, was the most persistent.

“As philanthropists, we were pouring tens of millions of dollars into climate solutions, but the fossil fuel companies were beating us,” says Dorsey. “They lobby for government inaction, promote science denial, greenwash their activities. We realized we had to target the industry itself.”

Dorsey also had a clear vision of the role philanthropic foundations would play in building a powerful fossil fuel divestment movement. For one thing, foundations could help legitimize what students were doing on campuses, she says. For another, they could help move money managers to create fossil fuel free investment products and, over time, demonstrate how a divested portfolio can outperform.

At the start of 2014, the RBF wasn’t quite ready to commit to divestment. The organization had focused in 2013 on replacing its OCIO, a move that was necessary to ensure that its prior commitment to boosting impact investing to its initial 10 percent target could come to fruition.

“It wasn’t clear that we had the bandwidth for the analysis and internal discussions needed to make the divestment commitment then,” Watson says. But Dorsey and others were pushing from the outside, as were members of the Rockefeller family, including Goodwin, who had been looking for ways to keep the fossil fuel industry in check since the mid-2000s, when as shareowners they had tried to force change at Exxon Mobil. Staff within the RBF were also pushing for divestment.

Agility took over management of the endowment in February of 2014. Everything was in place to make divestment possible. With the recognition that time was running out in the climate change battle, necessitating action to be taken, the RBF was able to arrive at the decision point and make the commitment.

In 2018, the RBF committed $14 million to an Ambienta fund that invests in resource efficiency and pollution control. Its portfolio companies include Amutec, which manufactures machines that make biodegradable and recycled bags, and AromataGroup, a producer of all-natural flavors and colors that respect the environment.

More than Symbolism

The divestment movement has expanded dramatically in the years since the RBF announced its decision to divest. When Stephen Heintz made that announcement in September 2014, he wasn’t speaking just for his organization and endowment, then around $850 million. He was speaking for 67 foundations from around the world with combined assets totaling $4.2 billion—reflecting the work Dorsey had done to rally foundations and philanthropies to the divestment cause.

As of early 2020, some 1,156 organizations and 58,000 individuals with more than $12 trillion in total assets have made a commitment to divest, in some fashion, from fossil fuels or to invest in climate solutions. That’s according to a tally kept by DivestInvest, a group founded by the Wallace Global Fund to encourage organizations to pledge to remove coal, oil, and gas from their investment portfolios and put their money to work to build renewable energy and advance other technologies necessary for a transition to a carbon-free economy.

In addition to reducing its own fossil fuel exposure, the RBF works actively to build the movement. Heintz, Rockefeller, Watson, and others regularly participate in private and public speaking engagements to share the lessons of the RBF's experience and encourage others to make the shift toward climate solution investments and away from fossil fuels. Program staff offer significant grant support to track and expand the list of investors ridding their portfolios of coal, gas, and oil stocks. And the RBF has made good on the commitment to be transparent about its progress, publishing data and updates about its remaining fossil fuel exposure, impact investments, and portfolio performance online.

The divestment movement has a growing influence on the world’s biggest capital markets. Though the movement began with educational institutions and philanthropic foundations, today fossil fuel divestment has been embraced by some of the largest pools of capital in the world, with insurers, pension funds, investment management firms, and banks now among the organizations signing on.

Ellen Dorsey on:

Why Divestment Works

“Divestment alone is not going to solve the climate crisis—that’s a legitimate point. But it is a necessary and effective step—and absolutely essential for building a movement that can take on a rogue industry. The divestment movement is how we've built relationships, developed leaders, capitalized solutions, and begun to take away the social license of fossil fuel companies. We’re making their stocks risky for a growing number of investors and their lobbying dollars toxic for politicians, allowing new policy ideas to actually move forward.”

Ellen Dorsey, executive director of the Wallace Global Fund, helped create DivestInvest Philanthropy, a coalition of groups that have committed to invest to address the climate crisis.

In January 2020, BlackRock, the world’s largest investment management company, which oversees about $7 trillion in investments, announced it would exit some investments related to coal production and put sustainability at the center of its portfolio construction and risk management offerings. In a letter to corporate leaders, BlackRock Chief Executive Officer Larry Fink declared that climate change has become the defining factor in companies’ long-term prospects. “I believe we are on the edge of a fundamental reshaping of finance,” Fink wrote.

The divestment lens doesn’t entirely fit BlackRock’s actions, since the firm manages that $7 trillion for its clients and doesn’t control how it’s invested. But the commitments the company has now made certainly are a bet that the demand for divestment and for investment products that are aligned with investors’ values is growing fast.

Following BlackRock’s announcement, in a development that may be the best indication yet of how the mood around fossil fuel investments is changing, the influential CNBC television personality Jim Cramer declared big oil companies to be a bad investment. “I’m done with fossil fuels,” he said on air on January 31. “We’re starting to see divestment all over the world.”

In subsequent days, Cramer compared fossil fuel companies to tobacco stocks and said many investors, including pension funds, are no longer willing to buy them. He said this wasn’t a political stand—he’s in the business of helping viewers make money and could no longer recommend the fossil fuel producers as a way to do that. Big oil companies “may just be on the wrong side of history,” he said.

There’s been an enormous shift in awareness in the capital markets in the more than five years since the RBF made its divestment commitment, and over the longer period in which the organization has been working to align its investing practices with its mission. Still, the urgency of the climate crisis compels many to consider what more can be done and who else can be brought along. In that effort, the RBF is committed to serving as an example of what’s possible.

“The RBF, as a symbolic actor and practical participant, has succeeded in divestment in an extraordinary fashion,” Lawson says. “This organization and its leadership were way ahead on divestment, and now everybody is talking about it and wondering whether they should do it.”

The RBF committed $15 million to a Generation Investment Management fund that includes a stake in Proterra, an electric bus manufacturer. The Proterra Catalyst E2 Max can travel up to 1101 miles on a single charge.

Conclusion

Making a Start

by Valerie Rockefeller, chair of the board of trustees

The RBF made its start toward fossil fuel divestment in 2014. Today, half a decade later, we can look back and see significant and measurable progress on our effort to get fossil fuels out of our portfolio and align our investing practices with our mission. We’ve been able to do what we set out to do, and we’re proud to share our experience.

Investments with exposure to the oil and gas business are now less than one percent of the holdings in the RBF endowment and will be entirely eliminated in the coming years. Coal and tar sands are essentially gone from the portfolio. Ridding our endowment of fossil fuels has helped rather than hurt our financial performance. This may not always be the case, but so far, the portfolio’s growth has exceeded expectations, beating the benchmark we use to measure our investing success and leaving the RBF in a healthy position to continue funding important programs for decades to come.

We were not the first to embrace divestment, but we were early. The movement we joined, and have helped nurture, is rapidly building momentum. When we set out on this path, the idea that fossil fuel reserves, a common basis for valuing energy companies, could become stranded was new and underappreciated. We leaned on this premise and the related concept that companies with oil and gas holdings were overvalued and risky and thus poor investments.

More recently, discussion of fossil fuels as stranded assets is often in the news. The idea that oil and gas reserves are mostly unburnable as we address the climate crisis is gaining currency, even if it still meets resistance on Wall Street and in some board rooms. Investors across the capital markets are grappling with the responsibility they bear for the money they put to work.

It’s become much easier, in the time we’ve been doing this, to find attractive clean energy investments. The reticence of some money managers, now faced with a demand for a fossil fuel free investment product, has in many instances been replaced by an inclination to serve the interests of investors who want to better align their money and their values. What’s more, the opportunities for investing in the transition to a clean economy have grown.

For the foundations and endowments that have resisted efforts to better match their investments to their missions or beliefs—there are still plenty—there are few reasons to wait. An organization doesn’t need to take the broad mission-aligned investing approach that the RBF has adopted, spanning fossil fuel divestment, impact investing, ESG investing, and active share ownership. But in that menu of options we have undertaken, which we have presented in this report, there are actions that any organization can take. It is essential to act now to avoid even more dire climate disruptions.

—March 2020

Copyright © Rockefeller Brothers Fund, May 2020. All Rights Reserved.

This report was researched and written by Robert Dieterich of 30 Point Strategies with editing and research help from RBF staff Geraldine Watson, Sarah Edkins Lien, and Emma Gatewood. Copyediting by Brianna Goodman. Graphic design by Constructive.

The authors extend special thanks to Chris Bittman, Mark Campanale, Ellen Dorsey, Neva Goodwin, Stephen Heintz, Tamara Larsen, Hugh Lawson, Michael Northrop, Tim O’Neill, Jameela Pedicini, Justin Rockefeller, Valerie Rockefeller, and Adam Wolfensohn for their time and insights. Additional thanks to Jeremy McKey for research assistance and Chase Lerner and Amita Schultes at Agility for data and image support.

The above is provided for information purposes only and is not an offer to sell, or a solicitation of an offer to purchase, any shares in any underlying pooled vehicles or managers named therein.